Understanding Mortgage Payment Fees

Home Loans, Mortgage Payments, Personal Finance

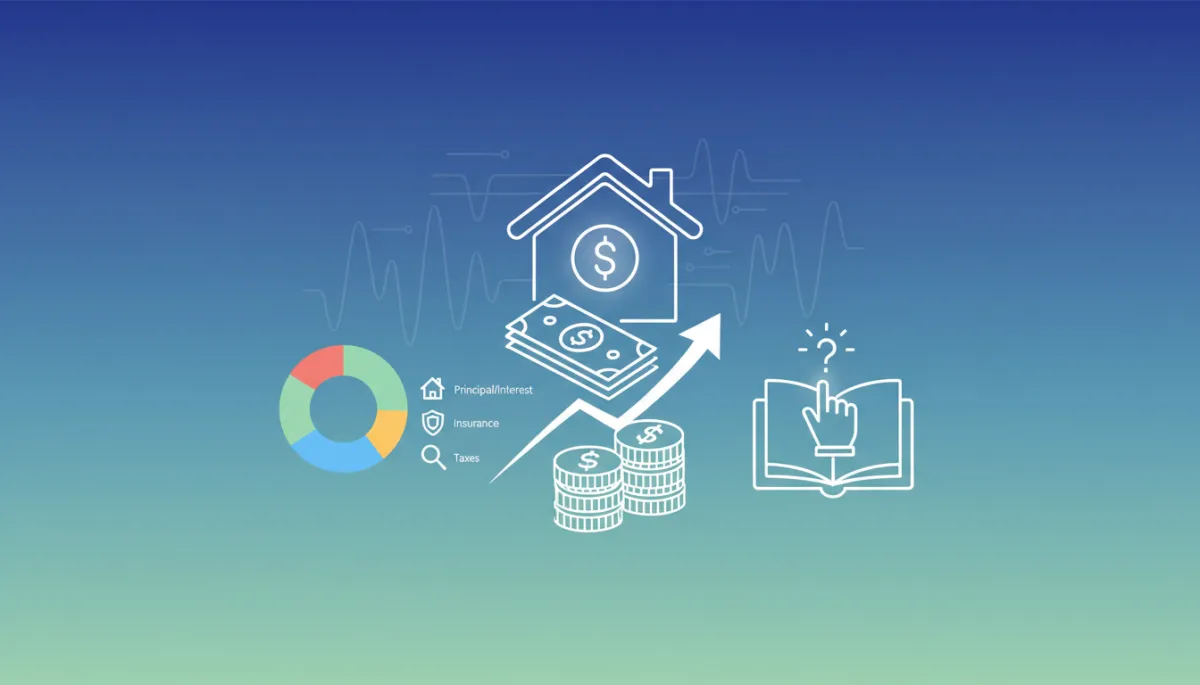

What Fees Are Included in a Mortgage Payment?

Understanding exactly what makes up your monthly mortgage payment can help you budget confidently, compare lenders more accurately, and avoid costly surprises over the life of your loan.

The Core of Your Payment: Principal and Interest

At the heart of every mortgage payment are two key components: principal and interest. The principal is the portion that goes toward paying down the amount you actually borrowed for the home. Over time, as you pay more principal, your outstanding loan balance shrinks and you build equity.

Interest, on the other hand, is the cost you pay the lender for borrowing that money. In the early years of a typical fixed-rate mortgage, a larger share of your monthly payment goes toward interest. As the loan matures, the balance shifts and more of your payment is applied to principal. Together, these two pieces are often referred to as the “P&I” portion of your mortgage.

Property Taxes Collected Through Escrow

Many lenders require an escrow account for property taxes. Instead of paying your tax bill in one or two large installments each year, your lender estimates the annual total and divides it into monthly amounts added to your mortgage payment. The lender then pays the tax bill on your behalf when it’s due.

This approach can make budgeting easier, but it also means your mortgage payment can change over time. If your local tax rate or your home’s assessed value increases, your escrow portion and therefore your total monthly payment may rise to cover the difference.

Homeowners Insurance and Additional Coverage

Lenders also typically collect money for homeowners insurance as part of your monthly mortgage payment. Just like with property taxes, these funds go into your escrow account, and the lender pays your insurance premium when it’s due each year. This protects both you and the lender if your home is damaged by events such as fire, storms, or certain types of accidents.

Depending on where you live, you may also see separate line items for flood insurance or other specialized coverage. If your property is in a designated flood zone or high-risk area, this additional insurance can be required and will increase the escrow portion of your payment.

Seeing principal, interest, taxes, and insurance clearly labeled demystifies your monthly payment.

Mortgage Insurance: PMI and Other Protection Fees

If you made a down payment of less than 20% on a conventional loan, your lender likely requires private mortgage insurance (PMI). PMI is designed to protect the lender if you stop making payments, and its cost is typically added to your monthly mortgage bill. The exact amount depends on factors such as your credit score, loan type, and down payment size.

Government-backed loans have their own insurance or guarantee fees. For example, FHA loans include a monthly mortgage insurance premium, and USDA and VA loans may include guarantee or funding fees. These charges are often spread across your payments over time, effectively becoming another fee embedded in your mortgage.

HOA Dues and Other Possible Add‑Ons

If your home is part of a community with a homeowners association (HOA), you’ll likely pay HOA dues separately from your mortgage. However, some homeowners choose to budget for HOA fees alongside their mortgage payment since both are ongoing housing costs. A few lenders or servicers may even allow you to combine the two into a single monthly bill, though this is less common.

You might also encounter smaller administrative fees from your loan servicer over time, such as charges for paper statements or optional services. While these are usually not part of the core principal, interest, tax, and insurance structure, they can still affect what you ultimately pay each month if you opt into them.

Why Your Payment Can Change Over Time

Even with a fixed-rate mortgage, your total monthly payment is not always static. While the principal and interest portion stays the same, taxes, insurance premiums, and mortgage insurance can all rise or fall. When your lender performs an annual escrow analysis, they may adjust your payment to ensure there’s enough money in your escrow account to cover upcoming bills.

Understanding each fee that’s included in your mortgage payment helps you spot these changes quickly, ask informed questions, and plan ahead. It can also reveal opportunities to save, such as shopping for a better insurance rate or eliminating PMI once you reach enough equity.

Take the Next Step: Get a Clear, Personalized Breakdown

Knowing that your mortgage payment covers principal, interest, taxes, insurance, and possibly mortgage insurance is the first step. The next step is seeing how those pieces look for your specific loan and goals. A personalized breakdown can show you where your money is going today and how small changes might help you save over the life of your mortgage.

If you’re ready to understand your payment in detail, compare options, or explore ways to reduce your monthly costs, don’t wait. Reach out to a trusted mortgage professional, request a full payment analysis, or start an online quote now. The more clearly you see every fee in your mortgage payment, the more confidently you can move toward the home and future you want.

📌 Ready to Talk Strategy in Warren County?

John Meier is a real estate agent in Warrenton, MO (63383) helping sellers in Warrenton, Truesdale, and Wright City.

Westplex Real Estate

📞 (636) 242-5365

🌐 JohnMeierSells.com